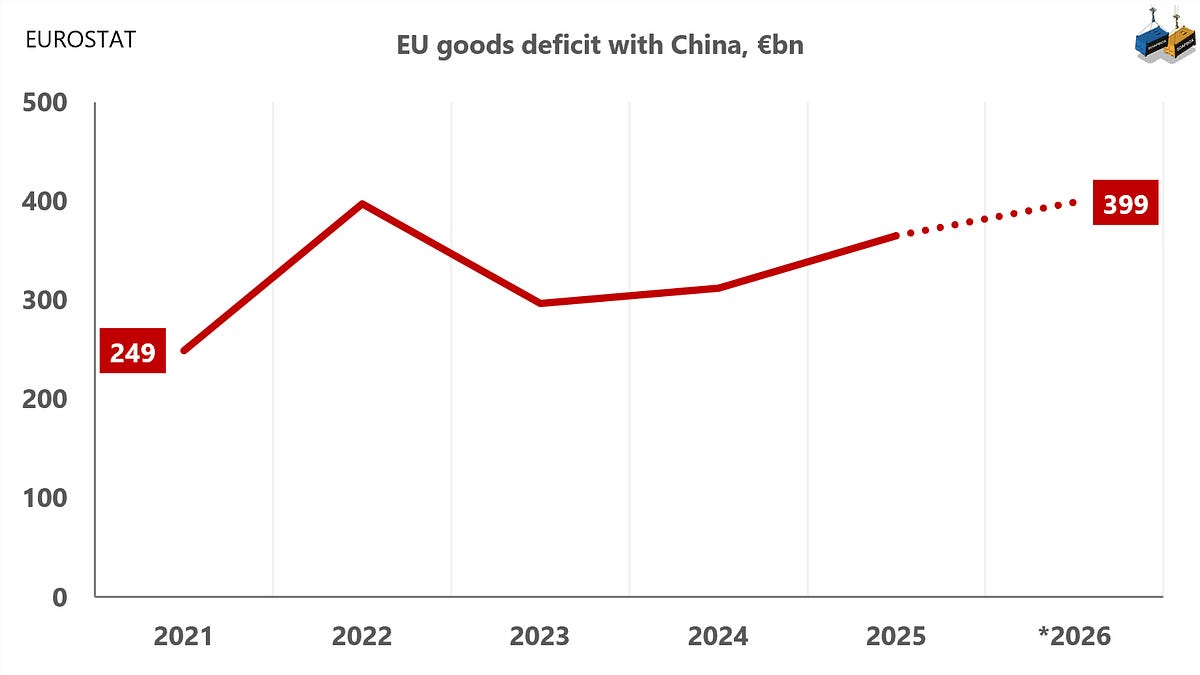

The Brussels mood is hardening, and the trade data explain why. On our estimate, the EU goods deficit with China is on course to reach almost €400bn in 2026, above the previous record set in 2022.

This is no longer just a trade-statistics story. It is becoming a political signal. The imbalance is large enough to matter at EU level, broad enough to appear across almost the whole Union, and difficult to dismiss as a problem of one sector, one country or one port.

In Jan-Apr 2026, almost every EU member state recorded a goods trade deficit with China. Ireland was the only exception, while Malta and Finland are essentially balanced.

The imbalance is not confined to one or two large economies. It appears across almost the entire Union.

![]()

On 18 and 19 June, EU leaders met in Brussels. Media reporting around the summit focused heavily on China, trade imbalances and the possibility of a harder EU line. The official European Council conclusions, however, read differently.

There is a striking disconnect between the political debate reported in the media and the heavily watered-down language of the formal communiqué.

Germany was by far the biggest contributor to the EU-wide deterioration in the trade balance with China between April 2025 and April 2026. The EU’s trade deficit with China widened by €2.9bn compared with a year earlier. Germany alone accounted for €2.0bn of that deterioration, roughly two-thirds of the total. The other 26 member states combined accounted for the remaining €0.9bn.

April brought more EU-China trade, but most of the growth flowed in one direction. EU exports to China barely moved, while imports from China rose more than €3bn, pushing the monthly deficit close to €32bn, or more than €1bn/day.

EU imports of electric and hybrid vehicles from China reached a record €6.0bn in Jan-Apr 2026, surpassing the previous high of €4.5bn in 2023. The rebound is striking because it comes after the introduction of EU anti-subsidy duties on Chinese electric vehicles. The composition of imports has changed, with hybrids becoming increasingly important, but the overall flow continues to grow.

Germany imported €324.1 million worth of electric and hybrid vehicles from China in April 2026, compared with €35.0 million a year earlier. Electric vehicles accounted for €174.6 million, while plug-in hybrids reached €130.0 million. Whether this proves to be a one-month spike or the start of a broader trend will become clearer when the May and June data are released.

The debate around Chinese vehicle imports has largely focused on electric cars. But the composition of imports is changing. In Jan-Apr 2026, EU imports of hybrid vehicles from China reached €3.2bn, overtaking electric vehicles at €2.8bn. The strongest growth is now coming from hybrids, particularly plug-in hybrids.

China is not only exporting more cars. It is exporting a new automotive architecture whose components are harder to track with traditional trade statistics. In the past, customs data offered a relatively clear picture: cars were recorded as cars, and many of their components were recorded as car parts.

That is becoming less true. A growing share of the value of an electric or hybrid vehicle sits in batteries, power electronics, sensors, semiconductors and digital systems. Many of those products are classified in customs categories that serve multiple industries, not just automotive.

As a result, the car remains visible in the trade data, but the supply chain behind it is becoming harder to isolate. China’s automotive footprint in the EU may therefore be larger than the traditional car and car-parts statistics suggest.

We also had time to take a quick look at the just-published May data from China Customs. The message is clear: the pressure is not over.

Exports recorded by China in May are already moving through the shipping pipeline. Some of those goods were still at sea when China registered them, and will only appear later in EU import records. That means the April numbers in EUROSTAT are not the end of the story. More Chinese goods are already on the way.

China’s May car exports to the EU, shown below, give a first glimpse of what is still coming.

China remains an important market for some European food products, but it is no longer the agrifood export engine it once appeared to be. EU agrifood exports to China fell from €6.2bn in Jan-Apr 2021 to €3.4bn in Jan-Apr 2026, a decline of roughly 45%.

The comparison is revealing. So far this year, the EU has exported around five times more agrifood products to the U.K. than to China, 2.6 times more to the U.S., and 1.4 times more to Switzerland. China remains a major trading partner overall, but in agrifood it is becoming a smaller piece of the EU export story.

EU imports from China are rising much faster in physical volume than in value. In Jan-Apr 2026, import value was up 4.0% year on year, while quantity rose by 12.8%. The average euro value per kg fell by 7.8%.

Currency may explain part of that fall, but not all of it. In April, the exchange-rate effect even points the other way. The broader signal remains: the EU is importing substantially more goods from China, but at a lower average value per kg.

The March-April data show the disruption clearly. EU imports from the Gulf fell in LNG, kerosene, renewable diesel, urea and conventional diesel. Crude oil was the exception, rising by 13% year on year.

That exception does not erase the Hormuz signal. Crude has more flexibility than some other Gulf exports: Saudi Arabia, the UAE and Oman offer at least some alternatives to the Strait of Hormuz.

Even if the latest agreement holds, the March-April data remain a warning. The Strait of Hormuz may reopen, but the speed and durability of that reopening are still political questions, not shipping questions.

Retail sales are still growing, but at a progressively slower pace. Average annual growth was 3.4% over the past five years, 3.2% over the past three years and 2.7% over the past two years.

The NBS interpretation of the May data leaves little doubt about the diagnosis: China’s supply side is still running ahead of demand. The English version calls this an “imbalance”. The Chinese text uses 矛盾, or contradiction. That word matters. In official Chinese political economy, a “prominent contradiction” is not a small technical mismatch. It is a structural problem that planners know they cannot ignore.

If domestic demand does not absorb the output, the pressure to sell abroad will remain.

Like this:

Like Loading…

Разгледайте нашите предложения за Български трактори

Иберете от тук

Българо-китайска търговско-промишлена палата