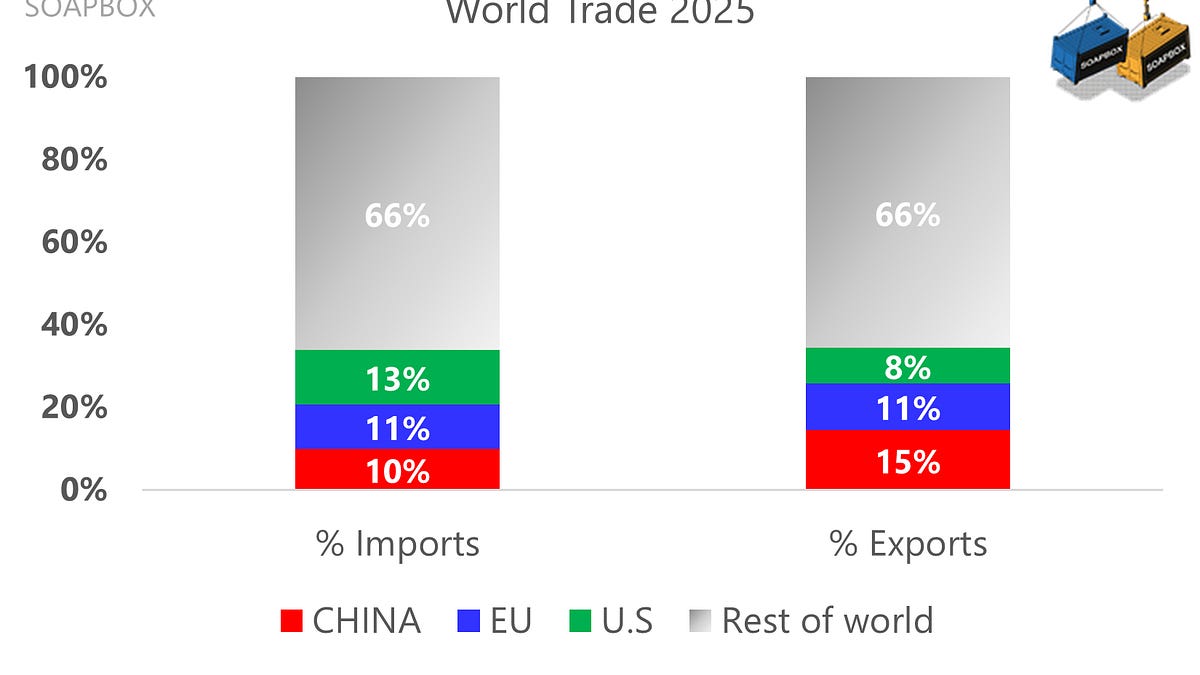

The chart explains why tariff politics often escalate fast. At 13% of global imports, the U.S. can hurt foreign exporters by taxing access to the U.S. market. At 15% of global exports, China is more vulnerable when others block, tax, or redirect demand away from Chinese goods. The EU is roughly balanced at 11% of both imports and exports, but it often becomes the spillover market as diverted goods and extra competition land in Europe.

As for Trump’s setback at the U.S. Supreme Court, expect rapid substitution. The administration is likely to keep tariff pressure intact with temporary authority under Section 122, including a higher global baseline of around 15%, while preparing slower but more durable routes under Sections 232 and 301, and other trade remedies.

Markets and trade flows will likely price in uncertainty more than relief. Even if a tariff line disappears, companies will assume it can return quickly in another form, or at a different rate.

In other words, the legal route may change, but the policy impulse remains the same.

In the meantime, the EU loses patience while China urges US to rescind unilateral tariffs

On the 4th anniversary of the invasion of Ukraine, the chart makes the geopolitical point without any adjectives. As the EU tightened its economic separation from Russia, China expanded its intake of Russian supply, especially in energy and raw materials, providing Russia with an alternative outlet and a continued flow of export income.

That trade is a proxy for geopolitics works here. The EU choice is visible as a collapse. China’s choice is visible as an expansion.

Whatever the diplomatic language, the trade arithmetic reads like a helping hand from China to Putin

The “EU surplus shrinks” headline now making the rounds is true at first glance, but it can imply a broad loss of EU competitiveness. The chart suggests a different story. In 2025, the EU’s overall goods surplus edges down (from about €141bn to €133bn), while its surplus excluding China actually rises (from roughly €453bn to €493bn).

The reason the total looks smaller is that the EU’s balance with China deteriorates further, effectively absorbing a larger share of the surplus the EU earns elsewhere.

That distinction matters, because it changes the diagnosis. A shrinking surplus driven by the rest of the world would point to a general export problem. A shrinking surplus driven by China instead signals a partner-specific imbalance: EU exporters struggle to expand in China, while imports from China remain strong. In other words, the EU’s external position is not “collapsing”; it is being reshaped by a widening China gap, even as the EU continues to perform strongly in other markets.

French wine sales to China were already falling, from about $1.1bn in 2017 to around $420m in 2025, the lowest level in 15 years. Recent talk of additional tariffs on French wine was not a formal policy decision. It came through a state-linked Chinese media account, a channel often used to signal Beijing’s political line before any official legal step. That is why the warning still matters: further restrictions could still hurt French producers, while causing limited disruption inside China.

In short, this is less about China’s demand for imported French wine and more about pressure in the wider EU-China tariff dispute.

In July 2025, the EU imposed anti-dumping duties on lysine imports from China. Lysine is a basic amino acid widely used in animal feed. A French producer now argues that the duties have been partly neutralised. According to the company, Chinese exporters responded by cutting their EU selling prices to absorb the tariff and keep post-duty landed prices competitive. If true, that would blunt the measure’s impact unless duties are adjusted upward.

In essence, this is an anti-absorption claim. The exporters did not “accept” the duty, they priced through it by lowering EU-facing FOB prices. France may be where the effect is most visible first, but the complaint is framed as EU-wide. Our quick check points in the same direction. EU-bound FOB prices fall more sharply than shipments to Russia, which we use as a rough control group and is the 4th destination by volume.

A subtle word change is spreading through China’s economic messaging. In past years, “around 5% growth” was almost always understood as real GDP growth. This year, however, more commentary and policy-adjacent reporting is explicitly talking about nominal GDP growth. It is a small shift in phrasing that points to a larger shift in priorities.

In China, wording that appears across multiple outlets is rarely random. It usually reflects a top-level emphasis that has become safe to repeat, with editors and commentators quickly converging on the same framing.

One driver is straightforward. Weak domestic demand has made growth feel thin, and soft prices have squeezed profits and expectations. But there is also a political horizon in the background, the 2035 objective of reaching the per-capita GDP level of “moderately developed” economies. That benchmark is ultimately about income levels and purchasing power, not just output volume, and nominal language aligns more naturally with that story. More importantly, weak prices and strong net exports can make real GDP look healthier than domestic demand really is, which is precisely why nominal growth is creeping into the official vocabulary.

The recent data make the shift visible. Across the 14th Five-Year Plan period (2021–2025), real GDP growth averaged about 5.3% per year, while nominal GDP growth averaged about 6.7%. Yet the pattern changed sharply at the end of the plan. Nominal growth fell below real growth in 2024 and 2025, consistent with a weak price backdrop. In the previous decade, by contrast, it was common for nominal growth to run well above real growth, sometimes by several percentage points.

Seen in that light, the nominal turn is not a technical curiosity. It reflects a reframing. Still, the rhetoric runs ahead of reality. Producer prices (PPI) remain negative, price wars persist, and overcapacity keeps margins thin in many sectors. The emphasis on nominal growth signals the virtuous cycle Beijing wants, stronger prices, profits and confidence, but it also reads like an aspiration. Converting that aspiration into outcomes will be harder than changing the wording. The real test is not whether the real-growth target shifts by half a point, but whether policy delivers a sustained lift in prices and nominal incomes.

When you read the China–IMF consultation documents, the fun is not in reading the IMF’s serious warnings to Beijing. The fun is in how Beijing dismisses the IMF’s analysis as a wrong interpretation.

China rarely accepts the framing. It usually argues that the IMF overstates the problem, misses context, or misattributes causes. China is especially combative on net exports, because accepting the IMF’s claim that China’s surplus creates adverse spillovers for trading partners would implicitly validate the idea that the surplus is policy-driven and should be reduced faster. So China contests the diagnosis rather than conceding the premise.

China’s script goes like this:

-

Exports were strong because of competitiveness and innovation, plus some front-loading.

-

Imports were weak because of external restrictions and lower commodity prices.

-

Exchange-rate policy was not used to gain an advantage.

-

Therefore, the IMF’s external-position call is overstated.

It works the same way when the IMF argues that China’s central bank lags peers in independence, adding that monetary policy decisions often reflect broader government objectives. China does not answer that point directly. Instead, it offers a labyrinthine reply, stressing that the authorities consider the monetary policy stance appropriately accommodative.

China Customs data points to a clear conclusion. China Japan trade remains large in absolute terms, but the relationship has shifted to a lower level than in 2021. Total trade falls from $371bn in 2021 to $322bn in 2025, a drop of about 13 percent. This is a downshift, not a break.

The main driver of that downshift is China’s import side. China’s exports to Japan move from $166bn to $157bn across the period, relatively contained. China’s imports from Japan fall from $206bn to $165bn, a much larger adjustment. If a reader wants one structural takeaway, this is it:

The bilateral slowdown is mostly about weaker Chinese purchases from Japan.

That also explains the balance story. China’s bilateral deficit narrows sharply from about $40bn in 2021 to single digits in later years. On paper, this looks like a healthier balance. In practice, the improvement comes largely from lower import volumes rather than stronger two way expansion. The relationship becomes more balanced, but also thinner.

However, the political backdrop has become more fragile: relations have deteriorated since late 2025. If current tension persists under Takaichi’s government, this “new normal” may not stabilise at current levels and could worsen into another leg down in bilateral trade volumes.

China’s government has been trying to reduce the country’s reliance on soybean imports. At one point, unofficial voices even argued that China would never import more than 100 million tonnes. So far, that ambition has not been met, and it remains unclear whether efforts to shift China’s huge pig sector toward alternative protein sources are delivering meaningful results.

For decades, MFN embodied the WTO’s core promise: equal treatment, no favourites. That principle is now back on the table because all major powers have pushed the system in different ways. Washington has used tariffs as geopolitical leverage, Brussels has widened trade-defence measures against what it sees as distortive competition, and Beijing has combined large-scale subsidies, industrial overcapacity, procurement asymmetries, and selective export controls in sensitive sectors.

In this context, WTO Director-general Ngozi Okonjo-Iweala’s remark that “the status quo is not enough” sounds less like routine reform and more like acknowledgement of a structural break.

For African economies, the effects are immediate: U.S. tariff pressure, only temporary relief through the African Growth and Opportunity Act (AGOA), and China’s broad tariff- and quota-free offers arriving at the same time. Yet the core imbalance persists.

Despite repeated pledges to expand African exports, China’s goods surplus with Africa widened sharply, rising from $6bn in 2018 to $103bn in 2025.

Peru’s politics just collided with a very non-Peruvian asset. Congress has removed interim president José Jerí after a scandal involving undisclosed meetings with a Chinese businessman, adding another twist to Lima’s familiar instability. This time, however, the backdrop is strategic. China’s COSCO holds 60% of the Port of Chancay, the flagship mega-project pitched as China’s Pacific logistics gateway into South America. The port was inaugurated in November 2024 with Xi Jinping “present” in Lima, though not physically on site.

The United States is treating this as more than domestic Peruvian drama. Ahead of President Trump’s 7 March Miami summit with aligned Latin American leaders, and just before his planned trip to Beijing, Chancay is likely to sit high on the agenda. The State Department’s 11 February warning on Xabout Peru’s ability to oversee the port made the point bluntly.

Our view is more prosaic. In the near to medium term, the numbers look tight. Peru–China trade is heavy on bulk minerals, and those shipments move through other ports, not a container terminal like Chancay. Add Peru’s weak road links, and the ramp-up becomes even harder.

That is why this project only really makes sense for a state-owned player with long patience (i.e. with China state support). A purely commercial operator would struggle to justify it on short-term cash flows.

Like this:

Like Loading…

Разгледайте нашите предложения за Български трактори

Иберете от тук

Българо-китайска търговско-промишлена палата