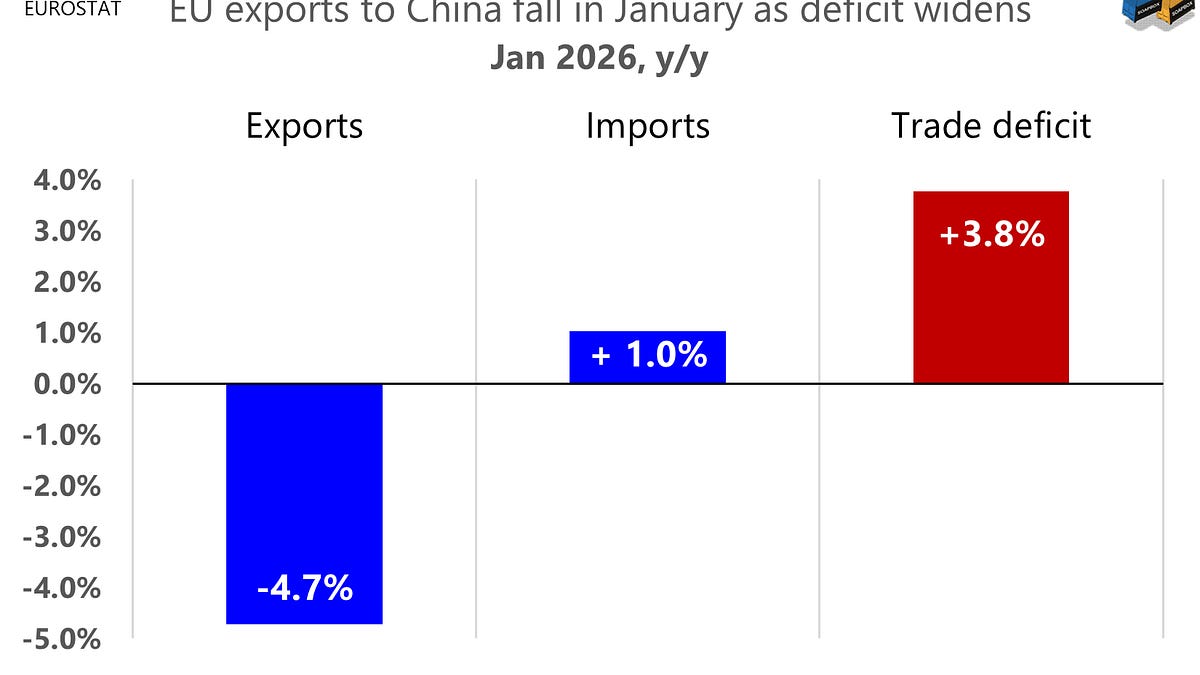

January brought a fresh widening in the EU’s trade gap with China. Exports fell 5%, imports rose 1%, and the deficit increased from €31.3bn to €32.5bn. Overall, EU exports were down 10% year on year, dragged lower by a striking near -28% plunge in exports to the U.S.

At first glance, January EU imports from China looked fairly soft in euro terms. Goods cleared at EU customs rose 2.4% by volume, but only 1.0% by value. Yet most of those goods were shipped in Q4 2025, when the euro was markedly stronger against the yuan than a year earlier. In other words, the euro figures understate the weakness.

Chinese new-energy vehicle exports to the EU are changing shape rather than retreating. In January, total imports rose 23% year on year, even as electric cars fell 38%, because plug-in hybrids doubled and non-plug-in hybrids more than tripled. The push into the EU market is continuing, but with a much stronger hybrid mix.

EUROSTAT’s January data show a sharp deterioration in the EU’s car trade balance with China. EU car exports to China fell 35% by value, dropping to €435mn from €665mn a year earlier.

The relative shift is just as striking. In January 2025, the value of EU car exports to China was still equivalent to about 90% of the value of EU car imports from China. One year later, that ratio had fallen to just 59%. In other words, the gap widened markedly in China’s favour.

The 2025 data confirms what was quickly foretold: once the U.S. signalled the end of de minimis exemptions for parcels, part of the flood was redirected towards the EU.

As a result, while exports by Shein, Temu and similar platforms to the U.S. fell by 25%, exports to the EU surged by 49%.

EU wine exports to China are now 87% below their peak nine years ago. To put that into perspective, January shipments were equivalent to barely one 12-bottle case per EU winery, or roughly two bottles per vineyard across the bloc. In other words, almost nothing. The downwards trend seems unstoppable, in January 2026 exports dropped 3.4% by value compared with a year earlier.

2025 was the year of the switch. Using Taiwan’s own reporting convention, the U.S. became Taiwan’s largest export market, overtaking Mainland China and Hong Kong combined. For 2026, we expect exports to both the U.S. and China to grow substantially, driven above all by semiconductors and the wider electronics supply chain. The more interesting question is not whether both will rise, but by how much. If U.S. demand keeps leading the current chip cycle, the post-2025 gap could widen further, even if China also rebounds.

Yemen’s Houthis are considering a Bab al-Mandab blockade in support of Iran. Recall that since Houthi attacks began, traffic through the Suez Canal has dropped by more than half from its 2023 peak.

According to Premier Li, international trade is a two-way choice that benefits both sides, and China has never sought to pursue a trade surplus.

Li presents China’s vast trade surplus as if it were simply the benign outcome of mutual market choice. But a surplus of this size and persistence does not emerge in a vacuum. It reflects an economic system that has consistently favoured production over consumption, industry over households, and export capacity over domestic absorption. China may not proclaim “trade surplus” as an official objective, but its policy mix has long pointed in that direction. Denying that is not an explanation. It is selective amnesia.

China’s state media is running a campaign to deny that there is anything problematic about the country’s huge trade surplus. In doing so, it implicitly falls back on an old argument associated with Friedrich List, the 19th-century economist who defended state-backed industrial catch-up.

We looked for total factor productivity (TFP) in the XV Five-Year Plan. It is there, but only in a very limited way.

The wording is familiar: TFP should “steadily improve.” This is not new language. It mirrors almost exactly the formulation used by Xi Jinping in October 2025, around the 4th Plenum and the drafting of the plan. In other words, the concept is acknowledged, but without any measurable commitment.

That marks a step back from the XIV Five-Year Plan. The previous plan also highlighted TFP, but with a clearer benchmark: productivity growth was expected to exceed that of the preceding period. It was not a hard number, but it was a reference point. In the new plan, even that disappears.

What followed likely explains the shift. Available evidence suggests that China did not deliver a meaningful improvement in TFP over 2021–2025 compared with 2016–2020. Productivity has remained under pressure from familiar factors: weak demand, overcapacity, and persistent misallocation. Against that backdrop, a softer formulation in the new plan is not surprising.

The implication is straightforward. The leadership is well aware of the TFP problem, but prefers to keep the language non-committal. “Steadily improve” signals direction without binding the authorities to a result. It preserves room to pursue growth through scale, industrial policy, and external demand, without being judged against a productivity benchmark that may prove difficult to meet.

Our reading is that this matters. Without a decisive improvement in productivity, and absent deeper reforms, the gap with the United States is unlikely to close. If anything, it is more likely to widen.

Like this:

Like Loading…

Разгледайте нашите предложения за Български трактори

Иберете от тук

Българо-китайска търговско-промишлена палата