In this issue, we’re pleased to begin a collaboration with the Mercator Institute for China Studies (MERICS) – Europe’s largest research institute focusing solely on the analysis of contemporary China and its relations with Europe. We look forward to join forces to provide you with the best insights on EU-China trade

2025 trade data will be out on 13 February

2025 trade data will be out on 13 February

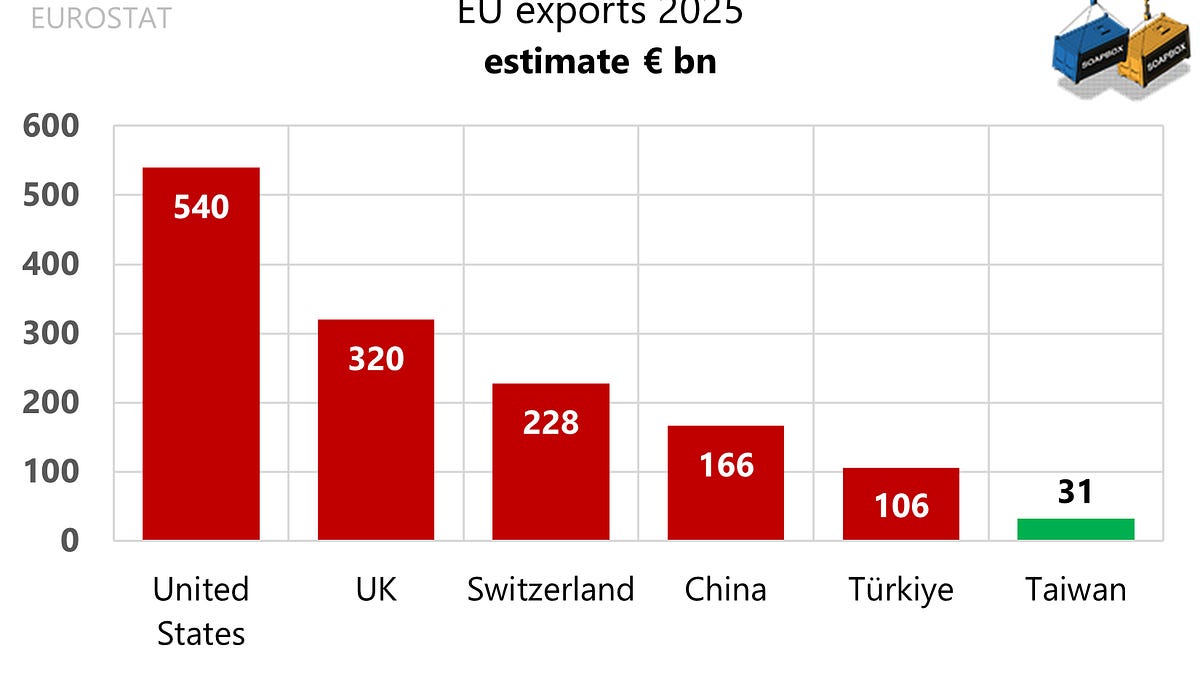

The chart puts that divergence in context. China is already well behind Switzerland as an export market for the EU, taking only around 7% of total EU exports.

Taiwan is there as a visual benchmark: the EU now exports only about five times more to the Chinese mainland than to Taiwan. Given the huge gap in economic scale and population, that ratio says a lot about where the trade landscape stands.

Jan–Nov 2025 shows broad weakness in EU exports to China, with only a small group of member states still posting year-on-year gains. The EU total is down 8%, and most large exporters are in negative territory, which largely drives the aggregate result. At the same time, the dispersion is striking. Denmark is up 19%, likely reflecting semaglutide-related API shipments. Several countries see steep drops, including Slovakia, where the Bratislava automotive hub appears to have been hit hard.

For readers who want more granularity than broad chapters, the concentration is even starker at product level. The EU exports 1,224 distinct HS4 product lines to China, yet just 87 of them account for three quarters of the total.

The data make it clear that the 2025 drop in EU exports to China is, above all, a car story. By November, car exports were down by more than €6bn, accounting for around 35% of the total decline. Add auto parts, down by more than €2bn, and cars plus parts together explain roughly 48% of the fall.

The two EU member states most directly affected are Germany and Slovakia.

Two categories did much of the work cushioning the 2025 decline. Both sit in the high-end aerospace supply chain, areas where China wants to build domestic capability, but still relies heavily on foreign technology, especially for engines.

Aircraft exports rose sharply. By November, EU shipments reached €5.7bn, up €1.9bn year on year (+49%). Aircraft engines followed the same pattern: EU exports of turbojets and turboprops climbed to €5.4bn by November, a net increase of €1.6bn (+43%).

In this area, China relies on three main suppliers: the EU (43%), the U.S. (43%), and the UK (3%).

Europe can be proud of its beverages. Few regions match the EU on quality, brand strength, and production standards. But the trade data with China tell a less flattering story. In 2025, the entire beverages chapter is down 18%, and in the overall export mix it is increasingly marginal for EU producers.

One comparison makes the point. China’s imports of copper scrap from the EU are worth about twice as much as its imports of EU wine and spirits combined.

Overall, agri-food is not the core story in EU exports to China. It accounts for roughly 6% of the total, and the biggest food lines are not “Mediterranean lifestyle” staples but industrial food preparations. In that sense, the often-promoted idea of a “vast Chinese consumer market” can be misleading when you look at what actually moves the trade numbers.

As mentioned above, copper scrap is a useful reality check. With a 1.1% share of total EU exports to China, it is not a footnote: China’s imports of EU copper scrap are worth about twice as much as its imports of EU wine and spirits combined. That gap points to a broader mismatch between what Europe would like to sell and what China is currently buying.

Semiconductor manufacturing tools have become geopolitical goods. The surge in EU exports to China in 2023–24 looks consistent with front-loaded buying as controls tightened and uncertainty rose. Taiwan follows a different rhythm, closer to investment cycles, but the rebound in 2025 also fits a broader shift towards concentrating advanced capacity in lower-risk locations.

Most EU supply in this segment comes from the Dutch firm ASML. In its 2025 results, ASML reported that China’s share of shipments fell from 44% in 2024 to 33% last year, while Taiwan moved the other way, doubling to 22% from 11% a year earlier.

This is trade data, but it is also policy and risk showing up in the numbers.

The EU and India have concluded negotiations for a major free trade agreement. But in trade terms, this is diversification, not replacement, at least for now. In 2025, EU–China total trade was about €735bn, versus €117bn with India. That is roughly a six-to-one gap. The deal can shift the trajectory at the margin, but it will not replicate China’s scale in the short term.

Electric bikes from China sprinted ahead early, petrol bikes kept grinding up, and by 2025 EU imports from China have them crossing the line together. Combined, the two categories top €2bn for the first time.

We expect a surge of petrol motorcycles from China into the EU in 2026. And yes, we mean it, at prices that undercut the market.

If China wants to reach the $4tn milestone, accelerating exports to the EU and the UK is the obvious lever. In 2025, exports were already up 8.4% to the EU and 7.8% to the UK. For EU policymakers, the implication is simple: Europe is on track to carry a larger share of the adjustment burden.

Frankly, there’s dark comedy in it: he’s raging at an outcome everyone saw coming.

Ports are now power, not just logistics. CK Hutchison’s planned disposal of 43 ports under long-term concessions has turned into a geopolitical negotiation, with Beijing pressing for a meaningful role for a state-owned player such as COSCO before anything can clear the approvals process.

Then Panama raised the stakes. On 30 January 2026, Panama’s Supreme Court ruled that the legal framework behind CK Hutchison’s concession to operate the Balboa and Cristóbal terminals at either end of the Panama Canal was unconstitutional.

Australia is the same story on a different map. On 28 January 2026, Prime Minister Anthony Albanese reiterated his commitment to bring the Port of Darwin lease back into Australian hands, and China’s ambassador warned of consequences.

Last time we checked, Chinese and Hong Kong-linked operators held interests in nearly 30 container terminals across the EU, typically through long-term operating concessions and/or equity stakes in individual terminals.

Like this:

Like Loading…

Разгледайте нашите предложения за Български трактори

Иберете от тук

Българо-китайска търговско-промишлена палата